Business segment review

Advanced Materials

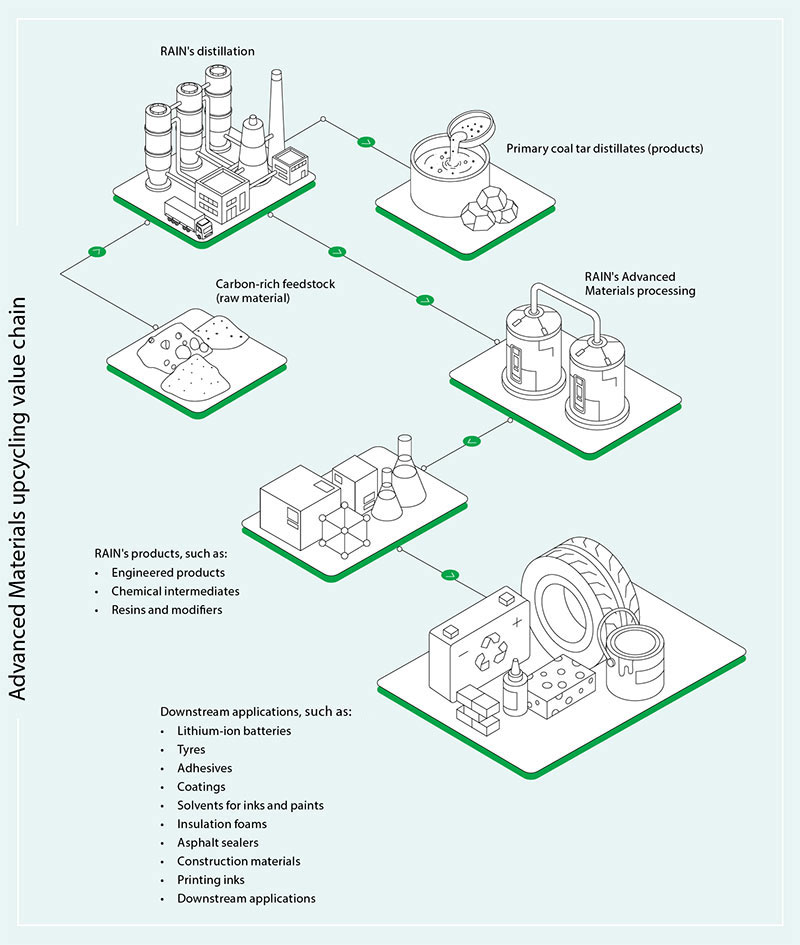

We are a global leader in advanced materials, transforming carbon, petrochemicals and raw materials into valuable products that are used in specialty chemicals, coatings, construction, automotive and petroleum industries.

Sales volume

Revenue from

operations

Contribution to

consolidated

revenue

Industries we serve

- Specialty chemicals

- Coatings

- Construction

- Petrochemical and others

- Energy storage

- Adhesives

| Product portfolio | |||

|---|---|---|---|

| Engineered products | Chemical intermediates | Resins | |

| Raw materials |

Coal tar and aromatic cracker residues, coal tar pitch and petroleum pitch | Naphthalene oil, crude benzene and cracker residues | Petro-based C9 feedstock (indene, vinyl toluene, etc..) |

| Manufacturing | Enhanced purification and physical separation processes significantly reduce the concentration of Polycyclic Aromatic Hydrocarbons (PAHs) and raise the softening point | Derived from our internal naphthalene oil production process, this material is further refined into downstream products such as phthalic anhydride | Cationic polymerisation and hydrogenation |

| End-industry applications |

PETRORES® and LIONCOAT® for energy storage materials; CARBORES® for carbon containing refractory and graphite products; and other advanced materials for asphalt sealer base products | Refined naphthalene for building and construction and other modifiers, phthalic anhydride for various downstream industries, benzene, toluene, xylene, solvents and fuel additives | Carbon resins, pure monomer resins, hydrogenated resins and phenolics |

| Production locations |

Belgium, Canada, Germany and Poland | Belgium and Germany | Germany |

We recorded improved volumes and profitability in the Advanced Materials segment over recent quarters, supported by seasonality and an enhanced product mix, even as energy and specialised chemical markets remained cost-competitive in Europe.

Capacity utilisation

The segment experienced a phased performance during the year, with an initial contraction followed by gradual recovery. Revenue and EBITDA declined early in the period due to lower volumes in the chemical intermediates and resins subsegments amid weaker demand and higher operating costs, partly offset by favourable Euro-Indian Rupee movements. Performance improved in subsequent quarters as volumes recovered, supported by seasonal demand and a refined product mix, while manageable energy costs in Europe aided profitability. Competitive pressure from Asian resin producers intensified during the year, requiring continued focus on pricing discipline and market share protection.

PETRORES® products and battery energy storage

The global lithium-ion battery anode market is projected to grow from US$19.06 billion in 2025 to US$81.24 billion by 2030 (CAGR 33.6%), driven by electric vehicle adoption and battery energy storage systems enabled by high energy density and fast-charging lithium-ion batteries. The shift toward silicon-enhanced and composite graphite anodes is improving performance, with graphite and silicon-carbon composites in negative electrodes, requiring solutions such as LIONCOAT® and PETRORES®. Supportive policies for zero-emission mobility and domestic battery manufacturing continue to drive capacity expansion. However, the industry faces supply chain concentration risks and rising regulatory scrutiny on emissions, waste and energy intensity.

We are leveraging increased volumes in engineered products and resins to drive revenue growth through focused product mix optimisation and seasonal demand capture.

We are managing energy cost pressures in Europe and stabilising feedstock inputs to sustain operational competitiveness.

The petroleum resin market is projected to grow from US$3.77 billion in 2025 to US$4.94 billion by 2030, reflecting a CAGR of 5.56%, supported by rising demand for hot-melt adhesives driven by expanding e-commerce packaging and increased use in rubber compounding to enhance tyre performance, particularly amid evolving electric vehicle requirements. Infrastructure expansion across Asia-Pacific, including India's US$87 billion investment pipeline, further supports consumption growth. However, market conditions remain sensitive to crude oil-linked feedstock price volatility and tightening environmental regulations, which are raising compliance costs and accelerating the shift toward low-VOC and more sustainable resin formulations.

In battery materials, we partnered with Northern Graphite to advance natural graphite anode solutions and expand the LIONCOAT® portfolio, targeting improved cycle life and faster charging performance.

In 2025, we advanced innovation in sustainable battery materials through a joint development initiative with Northern Graphite to convert natural graphite processing byproducts into high-performance, batterygrade materials. The collaboration integrates upstream feedstock control at the mine with downstream processing and electrochemical testing, aiming to maximise resource yield while reducing waste and carbon footprint. The development leverages our proprietary LIONCOAT® carbon coating technology at the Technology Innovation Centre in Hamilton, Canada, supported by an estimated investment of CAD 3.1 million, including a CAD 0.9 million grant under the Canada–Germany Collaborative Industrial Research & Development Programme.

Strategic focus areas for 2026

In 2026, we will advance next generation energy storage material product development in our new Technology Innovation Centre and collaborations with market partners to expand our presence in the battery anode material markets. Our focus will also include developing and integrating alternative raw materials to strengthen feedstock security and expand specialty product applications, supporting long-term growth in emerging energy markets.